The BRRRR calculator above runs the full math on your deal—purchase price, rehab, ARV, refinance, rental income, and expenses—and tells you exactly how much cash you’ll recover, what your monthly cash flow looks like, and whether the deal is worth doing.

BRRRR Calculator

🔄 BRRRR strategy: Buy undervalued property, Rehab to increase value, Rent for cash flow, Refinance to pull out equity, Repeat. Ideal for building a rental portfolio with less capital.

💡 Pro tip: Aim to refinance at 70-75% LTV to recover all or most of your initial investment. Positive cash flow and >10% cash-on-cash return are strong indicators.

No spreadsheet. No signup. Just clear numbers.

What Is the BRRRR Method?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It’s a real estate investing strategy built around one idea: recycle your capital instead of leaving it locked inside a property.

Here’s the cycle in plain terms:

- Buy a distressed property below market value—foreclosures, wholesale deals, properties that need work.

- Rehab it to increase the value above what you paid and spent combined.

- Rent it to a tenant and stabilize the income.

- Refinance with a cash-out loan based on the new appraised value (the ARV), pulling out most or all of your original investment.

- Repeat the process on the next property using the recovered capital.

Done well, BRRRR lets you build a rental portfolio without having to come up with a full down payment every time. The refinance does the heavy lifting.

How to Use the BRRRR Calculator

Enter your deal numbers in the fields above. Here’s what each section is asking for:

Acquisition & Rehab

- Purchase Price — what you’re paying for the property

- Closing Costs — typically 2–5% of the purchase price

- Rehab / Renovation Costs — your full repair and renovation budget, including contingency

ARV & Refinance

- After Repair Value (ARV) — estimated market value once renovations are complete

- Refinance LTV — most lenders allow 70–75% of ARV on a cash-out refi; 75% is the common ceiling

- Refinance Interest Rate — use current rates; rates in 2026 run roughly 7–8% for rental property cash-out loans

- Loan Term — 30 years is standard; shorter terms raise monthly payments but cut total interest

- Refinance Closing Costs — plan for 2–3% of the loan amount

Rental Income & Expenses

- Monthly Rent — use comparable rentals in the same market, not your best-case number

- Vacancy Rate — 5–8% is realistic in most markets; 10% if you’re being conservative

- Maintenance — budget 5–10% of rent annually for repairs and upkeep

- Property Management — 8–12% of rent if you’re not self-managing

- Property Tax and Insurance — check actual numbers for the property

Hard Money / Initial Financing

- Hard Money Loan % — lenders typically fund 70–90% of purchase plus rehab; the rest is your out-of-pocket

- Hard Money Interest Rate — current hard money terms run 10–15% with 1–3 points origination

- Months Held Before Refinance — most BRRRR rehabs target 2–4 months; add time for tenant placement before refinance approval

Once you hit Calculate, the tool shows you total cash invested, cash-out refinance amount, money left in the deal, monthly cash flow, and annualized cash-on-cash return.

Reading Your BRRRR Results

Total Cash Invested

This is your real out-of-pocket number during the buy and rehab phase—purchase down payment, hard money points, rehab costs above the loan, closing costs, and holding costs while the property sits vacant.

Cash-Out Refinance Amount

The amount the new loan puts back in your pocket after paying off the hard money loan. A full capital recycle means this number equals or exceeds your total cash invested. A partial recycle—recovering 80–90%—is still a strong outcome.

Money Left in the Deal

Cash invested minus cash recovered. Zero or negative means you’ve recycled all your capital and still own a cash-flowing asset. Positive means some of your money stays tied up in the property.

Monthly Cash Flow

Rent minus all expenses including the new refinance mortgage payment. Positive cash flow is the goal. If the number is negative, the deal doesn’t work as a rental regardless of how much equity you pulled out.

Cash-on-Cash Return

Annual net cash flow divided by money left in the deal. BRRRR investors typically target 10% or better. If you’ve recycled all your capital, this metric isn’t meaningful—what matters is the total return on a zero-cash-in-deal.

The 70% Rule for BRRRR Deals

The fastest filter for whether a property is worth analyzing:

Maximum Allowable Offer (MAO) = (ARV × 70%) − Rehab Costs

On a property with a $250,000 ARV and $40,000 in estimated repairs:

($250,000 × 0.70) − $40,000 = $135,000 maximum offer

That 30% margin covers financing costs, closing costs on both transactions, holding costs during rehab, and a buffer for surprises. If you pay more than the MAO, your refinance won’t return enough capital and you’ll leave money in the deal—or worse, take a loss.

What Makes a BRRRR Deal Work

1. Buy Below Market Value

BRRRR only works when the purchase price is low enough that post-renovation value significantly exceeds all-in costs. Distressed properties—bank-owned, probate, properties with deferred maintenance—are the hunting ground. You’re not looking for bargains on nice homes; you’re looking for problems you can solve at a price that leaves margin.

2. Accurate ARV Estimate

The ARV drives every downstream calculation. Overestimate it by 10% and your refinance falls short, leaving more capital in the deal than planned. Use comparable sales within the last 3–6 months, within half a mile of the subject property, with similar square footage and condition. When in doubt, be conservative.

3. Controlled Rehab Costs

Scope creep and contractor delays are the most common reasons BRRRR deals underperform. Every extra month in rehab adds another round of hard money interest. Get multiple contractor bids, build a 10–15% contingency into your rehab budget, and track actual spend against estimates weekly.

4. Refinance-Ready Rental

Most conventional lenders want to see a signed lease and 6–12 months of seasoning before approving a cash-out refinance. DSCR loans (debt service coverage ratio) are a faster path for some investors—they underwrite based on rental income rather than personal income and often don’t require seasoning. Factor your refinance timeline into the hard money holding period.

5. Positive Cash Flow After Refinance

The refinance mortgage payment is typically higher than the hard money interest you were carrying during rehab. Run the cash flow numbers with the permanent loan in place, not the bridge financing. If the deal doesn’t cash flow after refinancing, you’ve created a liability, not an asset.

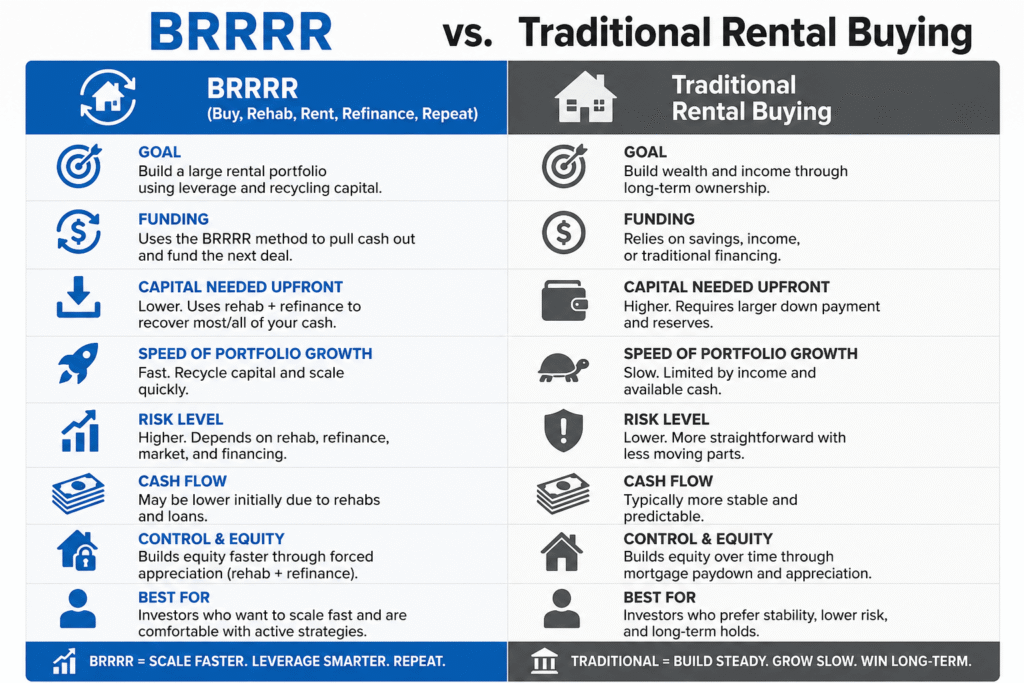

BRRRR vs. Traditional Rental Buying

| Factor | BRRRR | Traditional Purchase |

|---|---|---|

| Capital required per deal | Lower (recovered at refi) | Full down payment each time |

| Deal complexity | Higher | Lower |

| Equity position | Strong (bought below market) | Market price |

| Time to cash flow | 3–6 months minimum | Immediate |

| Scalability | High | Limited by capital |

| Risk | Higher (ARV, rehab, refi) | Lower |

BRRRR suits investors who want to scale a portfolio quickly and are comfortable with construction and project management. Traditional buying suits investors who want simplicity and immediate income without the rehab risk.

Common BRRRR Mistakes

Overestimating ARV. It’s the most expensive mistake in BRRRR. The entire strategy depends on the property appraising at or above your target. Run conservative comps, and if you’re new to a market, get a professional opinion of value before you close.

Underestimating rehab costs. First-time investors consistently underestimate what renovations actually cost. Labor, materials, permits, unexpected structural issues—they add up fast. Talk to local contractors before you make an offer, not after.

Ignoring refinance requirements. Not every lender will refinance an investment property after 4 months with a fresh tenant. Know your exit financing before you buy. Line up a lender who does DSCR or investment property cash-out loans before you need one.

Buying in weak rental markets. A property that won’t rent for enough to cover the post-refi mortgage payment isn’t a BRRRR candidate, regardless of how good the purchase price is. Check rental comps before you run the buy numbers.

Skipping reserves. BRRRR investors who recycle 100% of their capital often leave themselves with no cash cushion. If a HVAC goes out or a tenant stops paying, you need operating reserves. Build them into the deal analysis.

BRRRR Calculator vs. Spreadsheet

A BRRRR spreadsheet gives you flexibility—you can model custom scenarios and save multiple versions. The downside is setup time and the risk of formula errors that silently give you bad numbers.

This free BRRRR calculator is built for speed. You’re doing a quick deal screen to decide whether a property is worth deeper analysis. Get the key metrics in 60 seconds, then move to a spreadsheet if the numbers look promising.

Both tools are useful at different stages. The calculator filters deals. The spreadsheet closes them.

Frequently Asked Questions

What does BRRRR stand for?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It’s a real estate investment strategy that uses a cash-out refinance after renovations to recover the investor’s initial capital, allowing the same money to be deployed into subsequent deals.

How accurate is this BRRRR calculator?

The calculator uses standard real estate investment formulas and produces reliable estimates when you input accurate numbers. The two variables with the most impact—ARV and rehab costs—require market-specific knowledge. Use actual comparable sales and contractor quotes rather than guesses for the most useful output.

What LTV should I use for the refinance?

Most conventional lenders allow up to 75% LTV on a cash-out refinance for investment properties. Some lenders will go to 80%, but 75% is the standard to model for planning purposes. Using 70% gives you a conservative cushion.

Can I use this calculator for multi-family properties?

Yes. Enter the combined monthly rent for all units. For expenses, include all units’ operating costs. The ARV for multi-family is often calculated using a cap rate approach rather than comps—make sure your ARV estimate reflects how multi-family properties are actually valued in your market.

Do I need a hard money loan for BRRRR?

No, but it’s common. Hard money covers the purchase and rehab costs upfront when you don’t have the cash or don’t want to tie up other assets. Some investors use private money, self-directed IRA funds, or existing home equity lines. Enter the terms that match your actual financing.

What’s a good cash-on-cash return for a BRRRR deal?

Investors typically target 8–12% cash-on-cash as a minimum. But if you’ve recycled all or most of your capital in the refinance, cash-on-cash becomes less meaningful—you’re measuring the return on a very small (or zero) cash investment. In that case, focus on the absolute dollar cash flow and the equity position instead.

How is BRRRR different from fix-and-flip?

Fix-and-flip investors buy, renovate, and sell—taking a profit and moving on. BRRRR investors do the same buy-and-renovate steps, but instead of selling, they rent the property and refinance to pull out capital. BRRRR builds a portfolio of income-producing assets; flipping generates lump-sum profits but no ongoing income.

Use the BRRRR Calculator Free

The calculator at the top of this page is completely free—no account, no email, no credit card. Run as many deals as you need.

If you find it useful, explore our other real estate investing tools for deal analysis, cash flow projections, and financing comparisons.