Most people who discover Coast FIRE have the same reaction: I might already be closer than I thought.

That reaction makes sense — because Coast FIRE doesn’t require a massive portfolio. It requires a specific number invested early enough for compound growth to do the rest. The problem is that most people never actually sit down and calculate their Coast FIRE number. They see the concept, nod along, and go back to maxing out their 401(k) on autopilot without knowing whether they’ve already crossed the finish line.

This guide walks you through exactly how to calculate your Coast FIRE number — step by step, with real numbers. You’ll also see how Social Security benefits and pension income change the calculation significantly, often bringing your number much lower than you’d expect. And you’ll understand how Coast FIRE fits against Lean FIRE and Fat FIRE so you know which target actually applies to your situation.

By the end, you’ll have your number. Let’s get into it.

What Is Coast FIRE (and What Is Coast FI)?

The Core Idea in One Sentence

Coast FIRE is the point at which your invested portfolio is large enough that — left completely untouched — it will grow to fund your retirement by your chosen retirement age through compound growth alone.

No more retirement contributions required. You just need to earn enough to cover your current living expenses. The portfolio handles the rest.

Coast FIRE vs. Coast FI — Is There a Difference?

Technically, no. “Coast FI” and “Coast FIRE” refer to the same milestone. FI stands for Financial Independence; FIRE adds “Retire Early” to the acronym. Many people in the financial independence community use Coast FI to describe the concept without the “retire early” implication — because once you hit your Coast number, you’re not retiring, you’re just removing retirement savings pressure from your budget.

Use whichever term feels right. The math is identical.

How to Calculate Your Coast FIRE Number — Step by Step

Step 1 — Find Your Full FIRE Number

Before you can calculate your Coast number, you need your full retirement target. This is the total portfolio you’d need at retirement to withdraw from sustainably without running out of money.

The standard method uses the 4% safe withdrawal rate, a benchmark established by the Trinity Study — a long-running analysis of portfolio survival rates across 30-year retirement periods. The formula is simple:

Full FIRE Number = Annual Retirement Spending × 25

If you expect to spend $50,000 per year in retirement, your full FIRE number is $1,250,000. If you expect $60,000 per year, it’s $1,500,000.

Use your expected retirement spending — not your current spending. Most people spend less in retirement once the mortgage is paid off and children are grown, but healthcare costs often rise. A conservative estimate is 80–90% of your current annual spending.

Step 2 — Apply the Coast FIRE Formula

Once you have your full FIRE number, you work backwards to find how much you need invested today for compound growth to reach that target by retirement age.

Coast FIRE Number = Full FIRE Number ÷ (1 + Annual Return Rate) ^ Years Until Retirement

The key variable is years until retirement — the more years your money has to compound, the smaller your Coast number needs to be today.

For the annual return rate, use 7% as your baseline. That’s the inflation-adjusted historical average return of a broad US stock market index going back to 1926. It already accounts for inflation, so your result will be in today’s dollars — which makes it much easier to interpret.

Step 3 — Worked Example (Age 30, $50,000 Annual Spending)

Let’s put it together. Meet someone who is 30 years old, plans to retire at 65, expects to spend $50,000 per year in retirement, and uses a 7% real return assumption.

Step 1 — Full FIRE Number: $50,000 × 25 = $1,250,000

Step 2 — Coast FIRE Number: $1,250,000 ÷ (1.07)^35 = $1,250,000 ÷ 10.68 = $117,000

If this person has $117,000 invested at age 30 and never contributes another dollar, their portfolio reaches $1,250,000 by age 65. That’s Coast FIRE.

Run your own numbers with the Coast FIRE Calculator on ToolCalcPro — enter your age, retirement age, annual spending, and current savings to get your personal number instantly.

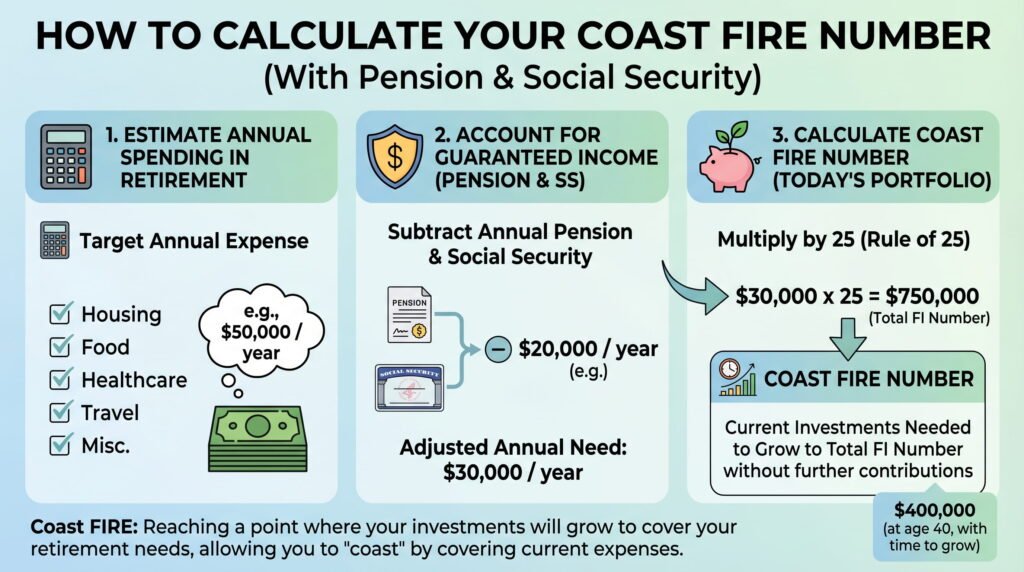

How to Calculate Coast FIRE with Social Security

Why Social Security Dramatically Lowers Your Number

Here’s what most Coast FIRE articles miss: Social Security reduces your Coast FIRE number significantly — sometimes by 30–50%.

Here’s why. Your full FIRE number is based on your expected annual spending in retirement. If Social Security covers part of that spending, your portfolio only needs to fund the remaining gap. A smaller retirement spending gap means a smaller FIRE number — and a smaller Coast number.

The Social Security Administration reports that the average monthly benefit in 2024 was approximately $1,907 — roughly $22,884 per year. For someone planning to spend $50,000 per year in retirement, Social Security covers nearly half of that.

Adjusted calculation with Social Security:

- Annual retirement spending: $50,000

- Expected Social Security benefit: $22,000/year

- Remaining gap your portfolio must cover: $28,000/year

Adjusted Full FIRE Number: $28,000 × 25 = $700,000

Adjusted Coast FIRE Number (age 30, retiring at 65, 7% return): $700,000 ÷ (1.07)^35 = $700,000 ÷ 10.68 = $65,500

That’s a Coast number of $65,500 instead of $117,000 — a 44% reduction just by accounting for Social Security. Many people in their late 20s and early 30s already have this much saved in their 401(k).

A Note on Using Social Security in Your Calculation

Use a conservative estimate. Your actual benefit depends on your earnings history and when you claim. Check your projected benefit at ssa.gov by logging into your Social Security account. Most planners use 75–80% of their projected benefit as a conservative assumption, since future benefit levels are subject to policy changes.

How to Calculate Coast FIRE with a Pension

Pension Income Works the Same Way as Social Security

If you have a defined benefit pension — common for teachers, military members, and government employees — it works exactly like Social Security in your Coast calculation. Subtract your expected annual pension income from your annual retirement spending before calculating your FIRE number.

The math is identical. The only difference is that pension benefits are often more predictable than Social Security, since they’re typically locked in based on years of service and final salary rather than dependent on national policy decisions.

Worked Example: Teacher with a Defined Benefit Pension

Meet a teacher, age 32, planning to retire at 62. She expects to spend $55,000 per year in retirement and will receive a $35,000 annual pension from her state’s teacher retirement system.

Remaining gap after pension: $55,000 − $35,000 = $20,000/year her portfolio must cover

Full FIRE Number: $20,000 × 25 = $500,000

Coast FIRE Number (age 32, retiring at 62, 7% return — 30 years): $500,000 ÷ (1.07)^30 = $500,000 ÷ 7.61 = $65,700

With a strong pension, this teacher’s Coast FIRE number is under $66,000. If she has that amount saved in her 403(b) today at age 32, she’s already coasted — she can stop retirement contributions entirely and focus purely on covering current expenses.

Teachers, firefighters, police officers, and federal employees are often surprised to discover they hit Coast FIRE years earlier than peers in the private sector, purely because of pension income.

Coast FIRE Number by Age — Reference Table

Your Coast number rises sharply with age because compound interest has less time to work. This table assumes a $1,500,000 full FIRE target (based on $60,000 annual spending) and a 7% real annual return, retiring at age 65:

| Current Age | Years to Retire | Coast FIRE Number |

|---|---|---|

| 25 | 40 years | ~$109,000 |

| 30 | 35 years | ~$152,000 |

| 35 | 30 years | ~$197,000 |

| 40 | 25 years | ~$276,000 |

| 45 | 20 years | ~$388,000 |

| 50 | 15 years | ~$545,000 |

Every five-year delay adds roughly 40% to your required Coast number. This table makes the case for starting early more clearly than any argument could. A 25-year-old needs $109,000. A 45-year-old needs $388,000 — for the same retirement outcome.

What Is My Coast FIRE Number? Key Variables That Change It

Return Rate Assumptions (7% vs. 5% vs. 10%)

The return rate you assume has a dramatic effect on your Coast number. Here’s how different assumptions change the result for a 35-year-old targeting $1,250,000 by age 65:

- 10% return (nominal, pre-inflation): Coast number ≈ $74,000

- 7% return (real, inflation-adjusted — recommended): Coast number ≈ $164,000

- 5% return (conservative, mixed portfolio): Coast number ≈ $289,000

Use 7% for your baseline. It’s inflation-adjusted, so your result is in today’s dollars. Using the nominal 10% makes your number look lower, but your retirement purchasing power is overstated. If you’re more conservative — holding significant bonds or nearing retirement — use 5–6%.

Retirement Age — Earlier Costs You More

Every year you move your target retirement age earlier, your Coast number increases. Earlier retirement means less compounding time and a longer withdrawal period, which requires a larger portfolio at retirement.

Moving from retiring at 65 to retiring at 60 typically increases your Coast number by 25–35%. If you’re targeting early retirement in your 50s, your Coast number jumps substantially — but it’s still almost always lower than full FIRE.

Spending in Retirement

Your annual retirement spending is the single biggest lever in the whole calculation. Cutting $10,000 from your projected retirement spending reduces your FIRE number by $250,000 and drops your Coast number proportionally. Track what you actually spend today — most people overestimate retirement expenses when they’re decades away.

Coast FIRE vs. Lean FIRE vs. Fat FIRE — Wich One Are You?

Coast FIRE is one of several milestones in the broader financial independence movement. Understanding where you sit among them clarifies which number you’re actually working toward.

Lean FIRE — Lower Target, Tighter Budget

Lean FIRE is full financial independence on a minimal budget — typically under $40,000 per year in spending, requiring a portfolio of $1,000,000 or less. It requires strict frugality in retirement and leaves little room for lifestyle upgrades, travel, or unexpected healthcare costs. It’s the fastest path to full FIRE for disciplined savers who are comfortable with a minimalist lifestyle.

A Lean FIRE calculator simply applies the same 4% rule to a lower spending number. If you plan to live on $30,000 per year, your Lean FIRE number is $750,000.

Fat FIRE — Higher Target, Generous Lifestyle

Fat FIRE is full financial independence with a generous lifestyle budget — commonly $100,000 or more per year in spending, requiring a $2,500,000+ portfolio. It takes longer to reach and requires either a high income, an aggressive savings rate, or both. The payoff is complete financial freedom without any lifestyle constraints in retirement.

A Fat FIRE calculator applies the same formula to a higher spending target. At $120,000 per year, your Fat FIRE number is $3,000,000.

Coast FIRE as the Middle Path

What makes Coast FIRE different from both is timing. You’re not trying to hit your full FIRE number now. You’re hitting a smaller target early — when compound growth has maximum runway — then stepping off the aggressive savings treadmill while your portfolio does the heavy lifting. It suits people who want financial security without sacrificing their 30s and 40s to extreme saving.

The three aren’t mutually exclusive. Coast FIRE is a milestone on the way to full FIRE — Lean, standard, or Fat. You hit Coast first, then coast the rest of the way there.

Frequently Asked Questions

What is a good Coast FIRE number?

There’s no universal “good” number — it depends entirely on your age, expected retirement age, annual spending, and whether you have pension or Social Security income. A 30-year-old planning to spend $50,000 per year in retirement with no pension might have a Coast number around $117,000. That same person with a $20,000 annual pension drops to roughly $65,000. Use the Coast FIRE Calculator with your actual inputs to get the right number for your situation.

Can I hit Coast FIRE in my 30s?

Yes — and it’s more achievable than most people realize. Someone who invests $20,000 per year from age 22 to 30 at a 7% real return ends up with roughly $230,000 by their 30th birthday. Depending on their spending target, that can be enough to coast to over $1,750,000 by age 65. The math consistently favors people who start early and invest aggressively in their 20s, even if they scale back significantly afterward.

Should I include Social Security in my Coast FIRE calculation?

You can — and it significantly lowers your number. The key is using a conservative estimate. Log into your SSA account at ssa.gov to see your projected benefit, then use 75–80% of that figure in your calculation to account for potential policy changes. Even a conservative Social Security estimate of $18,000–$20,000 per year can reduce your FIRE number by $450,000–$500,000 and your Coast number proportionally.

What happens if the market crashes after I hit Coast FIRE?

This is called sequence-of-returns risk. A significant market downturn in the early years of your Coast period — before your portfolio has had time to compound significantly — can push your retirement date back. The best protection is using conservative return assumptions (5–6% rather than 7%) so your number already has a buffer built in. Some people also maintain a small cash reserve equivalent to 1–2 years of expenses so they don’t need to touch investments during a downturn.

Your Coast FIRE Number Is Probably Lower Than You Think

Here’s the takeaway: once you account for Social Security, pension income, and the full power of long-term compounding, most people’s Coast FIRE number is significantly lower than their intuition suggests. Many people in their 30s and early 40s are already there without knowing it.

The only way to find out is to run the numbers. Use the Coast FIRE Calculator on ToolCalcPro — enter your current age, retirement target, annual spending, and expected Social Security or pension income. It takes about 30 seconds and shows you exactly where you stand.

You might already be coasting.

Have a specific scenario — dual income, rental income, or an unusual pension structure? Drop it in the comments and we’ll help you work through the numbers.