Most people assume boat loans work like car loans — three to six years, done. Then a lender quotes them a 15-year term and the whole mental model falls apart.

How long you can finance a boat depends on four things: the boat’s price, the boat’s age, your credit profile, and whether you’re taking a secured or unsecured loan. Get those factors right and you can lock in a term that keeps monthly payments manageable without paying more in interest than the boat is worth.

This guide covers every angle — new boats, used boats, bass boats, pontoons, motors, and slips — so you can walk into any lender conversation knowing exactly what to expect.

How Long Can You Finance a Boat?

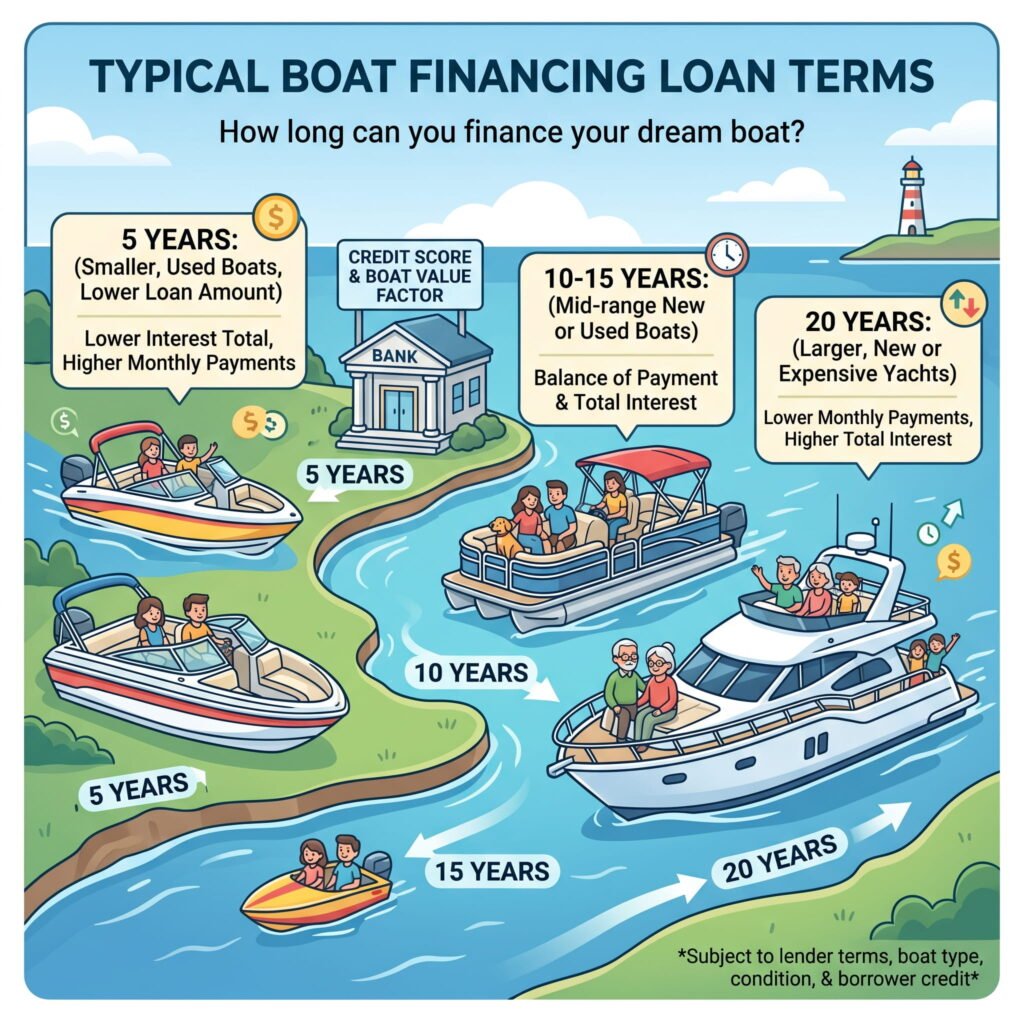

The direct answer: anywhere from 2 to 20 years, with most buyers landing somewhere between 10 and 20 years on a secured loan.

Standard boat loan terms in 2025

LendingTree data on closed boat loans puts the average term at 10 to 20 years, with an average interest rate of 10.03% in 2024. That’s based on real closed-loan data, not estimates.

Shorter loans (2–5 years) exist, but they come with much higher monthly payments. Longer loans (15–20 years) lower your monthly cost significantly — but stretch the repayment so far that total interest can exceed the boat’s original purchase price.

Why boat loans run longer than car loans

Boats last longer than cars. Discover Boating explains that decades ago lenders capped terms at around 10 years because older boats wore out fast. Modern boat construction changed that — a well-maintained vessel today can stay seaworthy for 25 years or more, and lenders have extended terms to match.

Midwest Water Sports puts the contrast plainly: the average car lasts about 8 years, while most 25-year-old boats are still on the water. That’s why a 20-year boat loan carries less collateral risk than an 84-month car loan — the asset simply lasts longer.

How Long Can You Finance a New Boat?

New boats get the most favorable terms. If your credit is solid, a new boat purchase is where you’ll see the full range of available loan lengths.

New boat loan terms by price range

Boat Trader breaks it down clearly by price tier:

- Under $50,000 — expect terms of 5 to 10 years

- $50,000–$200,000 — 10 to 15 years is typical

- $200,000 and above — terms up to 20 years, especially for well-qualified buyers

The average new boat costs around $42,000, which puts most buyers squarely in the 10–15 year window, not at the 20-year ceiling.

What makes new boats eligible for longer terms

Lenders are lending against the boat as collateral. A new boat holds its value longer, has no unknown mechanical history, and is unlikely to need major repairs in its first few years. That makes it a lower-risk asset for the lender — and lower risk translates directly into longer available terms for the buyer.

How Long Can You Finance a Used Boat?

Used boats come with shorter timelines, but that doesn’t mean you’re stuck. The key variable is the boat’s age, not just its price.

How boat age affects your loan term

Wavve Boating puts the used boat window at 5 to 15 years, with some lenders extending to 20 years on newer, high-value used vessels. The older the boat, the shorter the term you’ll be offered — because the lender doesn’t want to be holding a 30-year-old vessel as collateral on a loan that still has 10 years to run.

Boatsetter notes that some lenders won’t finance boats past a certain model year at all. Others will finance older boats but only if the loan amount is large enough — you’re unlikely to find a lender willing to stretch a $10,000 loan on a 15-year-old boat over 15 years.

Used boat loans for older models (2006, 2007, 2008 boats)

A boat from 2006, 2007, or 2008 is now roughly 17–20 years old. Most lenders cap the term on a boat that age at 5 to 7 years — or decline entirely unless the vessel is high-value and in documented good condition.

If you’re shopping a boat this old, get a professional marine survey before applying. It protects you from hidden mechanical issues and gives the lender confidence in the collateral. Many used boat deals fall apart after a survey because a clean exterior doesn’t always reflect what’s underneath.

Loan terms by boat type

Not every boat category is treated the same. Type and use case matter — here’s what to expect across the most common categories.

How long can you finance a bass boat?

Bass boats typically run $20,000–$60,000 new. At that price range, expect loan terms of 5 to 10 years, occasionally stretching to 12 years depending on the lender and total loan amount. Bass boats are smaller vessels with shorter expected lifespans than large cruisers or luxury yachts, which keeps the available terms on the shorter end.

A $35,000 bass boat with a 10% down payment means financing $31,500. At a 5-year term, your monthly payment runs noticeably higher than at 10 years — but your total interest paid drops significantly.

How long can you finance a pontoon boat?

Pontoon boats are among the most commonly financed vessels. Newer pontoons in the $40,000–$80,000 range typically qualify for 10 to 15 year terms. Discover Boating notes that some lenders treat multi-hull boats differently from standard powerboats, so it’s worth asking your lender upfront whether pontoons fall under standard or specialized loan guidelines at their institution.

How long can you finance a boat motor?

A standalone boat motor is a smaller purchase — typically $5,000–$20,000. Most lenders won’t extend motor-only financing beyond 5 to 7 years because the loan amount is small and the collateral depreciates quickly. Some buyers finance a motor through a personal loan rather than a marine loan to avoid collateral requirements — though unsecured personal loans generally carry higher interest rates than secured marine loans.

How long can you finance a boat slip?

Boat slip financing sits in its own category. Slips are often financed like commercial real estate or long-term leases rather than standard marine loans, and terms can run 10 to 20 years depending on whether you’re purchasing a deeded slip or a long-term ownership interest. Most general lenders don’t carry a standard slip product — a marine-focused lender or credit union with experience in slip transactions is your best starting point.

What actually controls your loan term?

Lenders don’t assign a number at random. Four main factors drive every term decision.

Loan amount

This is the biggest lever. Right Boat explains that lenders use loan size as a primary gating factor — a $10,000 loan won’t qualify for a 20-year term no matter how strong your credit is. Larger loans unlock longer terms because lenders are more comfortable spreading a bigger balance over time.

As a rule: the higher your loan amount, the more term flexibility you’ll have.

Credit score

First Alliance Credit Union sets the practical threshold at 680 or higher for a solid range of term and rate options. Borrowers above 750 often get to name their preferred term rather than accepting whatever the lender offers.

Elite Direct Finance confirms the flip side: lower credit scores push buyers toward shorter terms with higher monthly payments — the opposite of what most buyers in that situation want. If your score is below 680, spending a few months improving it before applying can meaningfully change what terms you’re offered.

Down payment

Most lenders require 10% to 20% down on a boat loan. A larger down payment reduces your loan balance, which can either shorten the term you need or get you a better rate on the same term. It also protects you from going underwater — owing more than the boat is worth — in the first few years of ownership.

Secured vs. unsecured loans

The loan type sets a hard ceiling. Right Boat lays it out clearly: a secured loan — where the boat itself is collateral — can run up to 20 years. An unsecured personal loan for a boat purchase tops out at 5 to 7 years. If you need a longer term to make the payment work, a secured marine loan is the only path to get there.

How to choose the right boat loan term

Knowing what’s available and knowing what’s smart for your budget are two different things.

Short term vs. long term — which costs less?

A shorter term always costs less in total interest. The monthly payment is higher, but you exit the loan faster and pay significantly less for the privilege of borrowing.

Here’s a concrete example from LendingTree: borrow $37,800 at 10.03% APR. On a 20-year term, the monthly payment drops to something manageable — but the total interest paid over the life of the loan can easily exceed the original purchase price. Knock that term down to 10 years and you pay far less overall, with a higher but still workable monthly payment.

The right term is the shortest one where the monthly payment still fits comfortably alongside your full cost of ownership — which includes insurance, storage, maintenance, fuel, and registration fees on top of the loan itself.

Use a calculator before you apply

Run the numbers before you sit down with a lender. Plug in three different terms — 7, 10, and 15 years — and compare the monthly payment against total interest for each. You’ll often find that a term two or three years shorter saves thousands in interest for only a modest increase in your monthly payment.

If you’re also weighing how a boat purchase fits into your broader financial goals — retirement savings, debt payoff, investment contributions — the Coast FIRE Calculator on ToolCalcPro can help you figure out whether your current savings are on track before you add a new loan to the picture. It takes two minutes and can change how you think about the right term length.

The bottom line

How long can you finance a boat? Up to 20 years on a secured loan for a new, high-value vessel — and as few as 2 to 5 years on a small used boat or standalone motor.

Three rules to keep in mind: larger loans unlock longer terms, newer boats get better terms than older ones, and a higher credit score puts you in control of which term you take. Run your numbers across multiple term lengths before committing — the difference between a 10-year and 15-year loan on the same boat can add up to thousands in extra interest over time.

Want to see how a boat purchase fits into your overall financial picture? Use the Coast FIRE Calculator on ToolCalcPro to check whether your current savings are on track before you take on new debt.

Have a question about your specific situation? Drop it in the comments — happy to help you work through the numbers.